This site is part of an affiliate sales network and may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This relationship may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Zachary Abel is also a Senior Advisor to Bilt Rewards. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

Got crappy credit? FICO may just boost your score

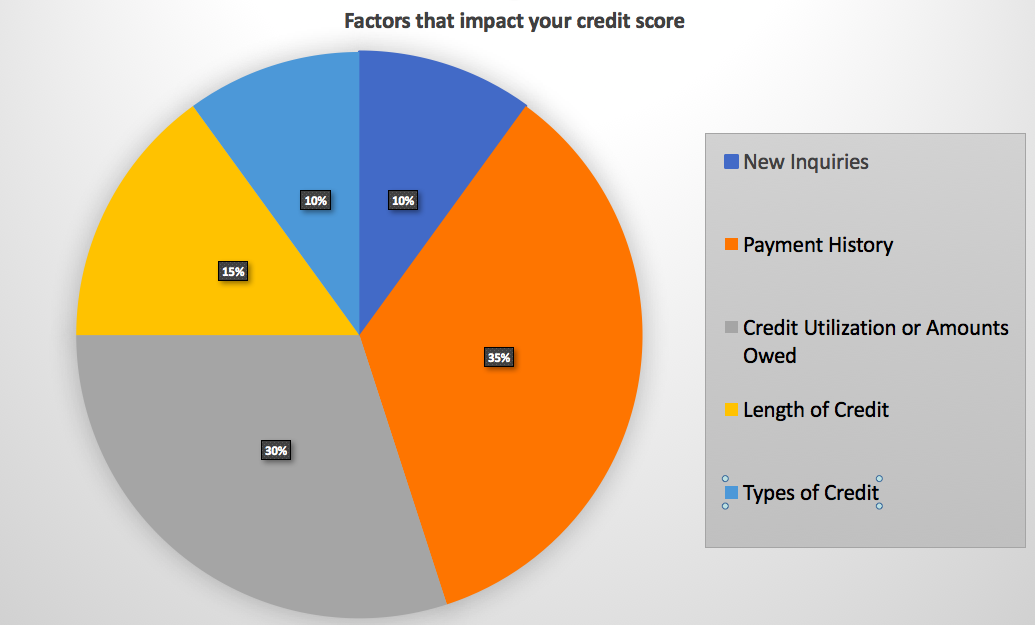

According to ZeroHedge, FICO will start weighting borrowers who have unpaid medical bills on their credit report with less severity. What does this mean? Nearly 12 Million people may get a boost on their credit score of up to 25 points. FICO did something similar 4 years ago when they started removing bills that had been paid after it had gone to collections: rather than it taking the normal 7ish years to roll off of credit reports, they eliminated the data from credit score calculations. WHAT?! If I was a lender I think I should have the data that shows that someone didn’t pay back their bill, even if it went to collections. Collection agencies buy debt at a discount…so future lenders should have access to this information for risk assessment. If you can’t properly assess risk, how can you set prices, properly lend? Market manipulation increases the odds of seismic, black swan events.

Quoted by ZeroHedge:

“It’s going to make someone who has poor credit look better than they should,” said John Ulzheimer, a credit specialist and former manager at Experian and credit-score creator FICO.

“Just because the lien or judgment information has been removed and someone’s score has improved doesn’t mean they’ll magically become a better credit risk.”

The road to hell is paved with good intentions:

How could this help lenders? Potential borrowers who shouldn’t be credit worthy are extended credit intended for less-risky borrowers because the system now cloaks bills gone to collection. Black Swan events happen because free markets aren’t allowed to work properly. There should be ebbs and flows. Think back to the banking crisis of 2008/9 – Mortgage Backed Securities were being packaged with ratings much higher than was representative of the underlying asset’s risk of default. They boosted the system to make money. THIS – feels like very much of the same. They want more people to be extended credit regardless if it will increase the odds of default.

No one would trust a store that prices and sells a flawless bushel of apples only to discover that all of the apples underneath the topmost were in fact rotten.

I have first hand experience…

I have had first hand experience with medical bills negatively impacting a credit score. Over 10 years ago I visited a doctor and was told they’d mail me my co-pay: $5. Unfortunately when they did, I had moved and forgot to forward my mail. I only found about it when I was inquiry about an auto lease and didn’t have top tier credit. I’d paid every bill I’d ever received. I was wrong – That $5 medical bill dropped my score between 100-150 points. HOLY $&%!!!!! It was a good lesson to learn in my early 20s. It wasn’t that I didn’t want to pay the bill or have the means, but rather made a mistake. This new process FICO will adopt is clearly targeted at people with similar intentions as myself – creditworthy and made a stupid mistake, but will pay the bill. However, I don’t think that’s always the case. And lemme tell you – it sucked to have my score drop that much, but I deserved to have it happen. I also check my score ALLLLLL the time now, forward my mail, and make sure my bills are paid. Even with that on my account, my score popped over 750 roughly a year later. This was over 10 years ago, but it was a good lesson learned.

I’ll leave you with one final quote from the article. By 2018 medical related claims will be removed after they’ve been paid and rectified.

Such changes might help borrowers and could spur additional lending, possibly boosting economic activity. But it could potentially increase risks for lenders who might not be able to accurately assess borrowers’ default risk.

Consumers with liens or judgments are twice as likely to default on loan payments, according to LexisNexis Risk Solutions, a unit of RELX Group that supplies public-record information to the big three credit bureaus and lenders.

TWICE AS LIKELY? Sheesh!

Am I being overly harsh? There is far more information in it and a WSJ article.

Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved, or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.