This site is part of an affiliate sales network and may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This relationship may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Zachary Abel is also a Senior Advisor to Bilt Rewards. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

How credit utilization can kill your credit score

I wrote an article at the end of 2015 ( ” A personal account of how Credit utilization affects your score ) that detailed the HUGE impact utilization can have on your credit score. Since then, MonkeyMiles has gone from Prior2Board and now BoardingArea and I thought it would be responsible, helpful, informative, etc to get the word out to a much bigger audience: DO NOT CARRY A BALANCE. Utilization is a KILLER. In my case, I had taken advantage of a deal whereby you could fund a bank account with a credit card. I was technically carrying a balance until my statement close, but paid it off immediately after. When your statement hits…you will see that balance on your credit score and your score will DROP – big time. This is how credit utilization can KILL your credit score

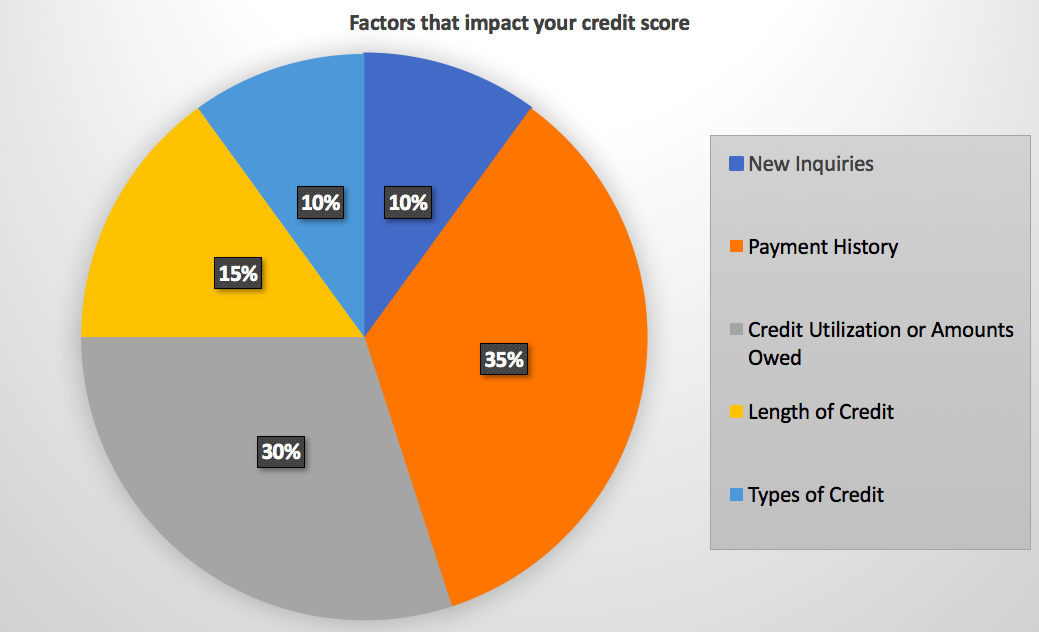

Just a quick reminder, 30% of your score is utilization – That’s HUGE

- Utilization is how much of your credit line you’re currently using. AGAIN this represents 30% of your credit score

- This could be that you’ve built up a balance and are working on paying that off, or as in my case, I simply charged a large amount and didn’t pay it off before the statement hit. That BALANCE was reported and NEGATIVELY impacted my score.

This example is from 2015 when Citi allowed bank accounts to be funded with credit cards

I dropped my cash advance limit to $0 on my Barclay Aviator Red ( so I knew I’d avoid fees) and funded a Citi Gold account with $25k from the card. I got hit with a 25k charge and had 25k in my bank account. The reason?

At the time, you could earn 50k AAdvantage miles opening an account, funding it, and doing a couple payments, debit card payments, etc. I used the money that was deposited into the account to pay off the credit card so I was merely nesting the money to earn the points. I netted 75k AA miles for doing this, but noticed a GIGANTIC drop in my credit score.

- 25k on the Barclay Aviator Red and 50k with the CitiGold account

That one, 25k charge hit my credit hard…HOLY COW! A Big drop! 80 points! I dropped from Top Tier credit to 2nd tier.

To put this in perspective…at this time I had almost 250k in total “depth of credit” so we’re talking a 10% utilization rate if you apply 25k over the total line. Not that high…the problem is it used almost 100% of one line, Barclay’s, which was a little over 30k when I did it.

When you pay your debts…your credit score JUMPS

I had already paid the card off in full when I checked my score – this drop purely reflected the increased utilization reported to the agencies…It said it would update again on the 15th so I waited a week to see how much it would recover. It actually recovered ABOVE where it had originally fallen from.

The biggest lesson that I learned was the impact of utilization

My credit didn’t drop because my overall utilization went down – how I had suspected – but went down because of the individual bank’s reporting on utilization: that had a MAJOR impact on my credit. My overall credit line at Barclay was 30k – when I used up 25k on funding, my utilization rate SKYROCKETED and both Experian and Transunion took notice. This utilization rate is egregiously high and should considerably drop my credit if it represented me as a borrower…the problem was it didn’t accurately reflect my OVERALL utilization, but just an individual bank’s utilization. That’s worth paying attention to.

3 big things to take home with you

- If you really need to have an outstanding credit score every month…pay off a big purchase before the account statment closes for the month, it won’t be reported.

- Utilization reported by a bank is what impacts the score more than the overall, collective utilization

- If you need to make big purchases, put them on a business card. Those purchases don’t show up on a personal credit report.

- DON’T CARRY A BALANCE

Hope this helps!

PS – Interested in a business credit score? – check out this article at lendgenius that explains this in more detail.

Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved, or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.