This site is part of an affiliate sales network and may earn compensation when a customer clicks on a link, when an application is approved, or when an account is opened. This relationship may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Zachary Abel is also a Senior Advisor to Bilt Rewards. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

Medical Travel Insurance

Personally, I like to make sure I have some sort of medical coverage when I’m traveling overseas. Certain U.S. based health insurance policies do provide coverage, and a couple of my credit cards also provide emergency medical evacuation, but I like to have my bases covered. I use various cards for various travel purposes, and I have a sneaking suspicion that if there is a reason for that Emergency Medical Evacuation to not be covered, the credit card company will find it. I usually use Allianz for travel insurance and discovered something a few years back, while on a trip to Australia, that you CAN buy travel insurance after you’ve departed. It’s not even that expensive…so if you’re currently on a trip, or realize you forgot, like I did, you can cover your trip after you’ve left.

I’ve also purchased year long plans with GeoBlue ( I’ve used the Trekker plan ).

What’s covered?

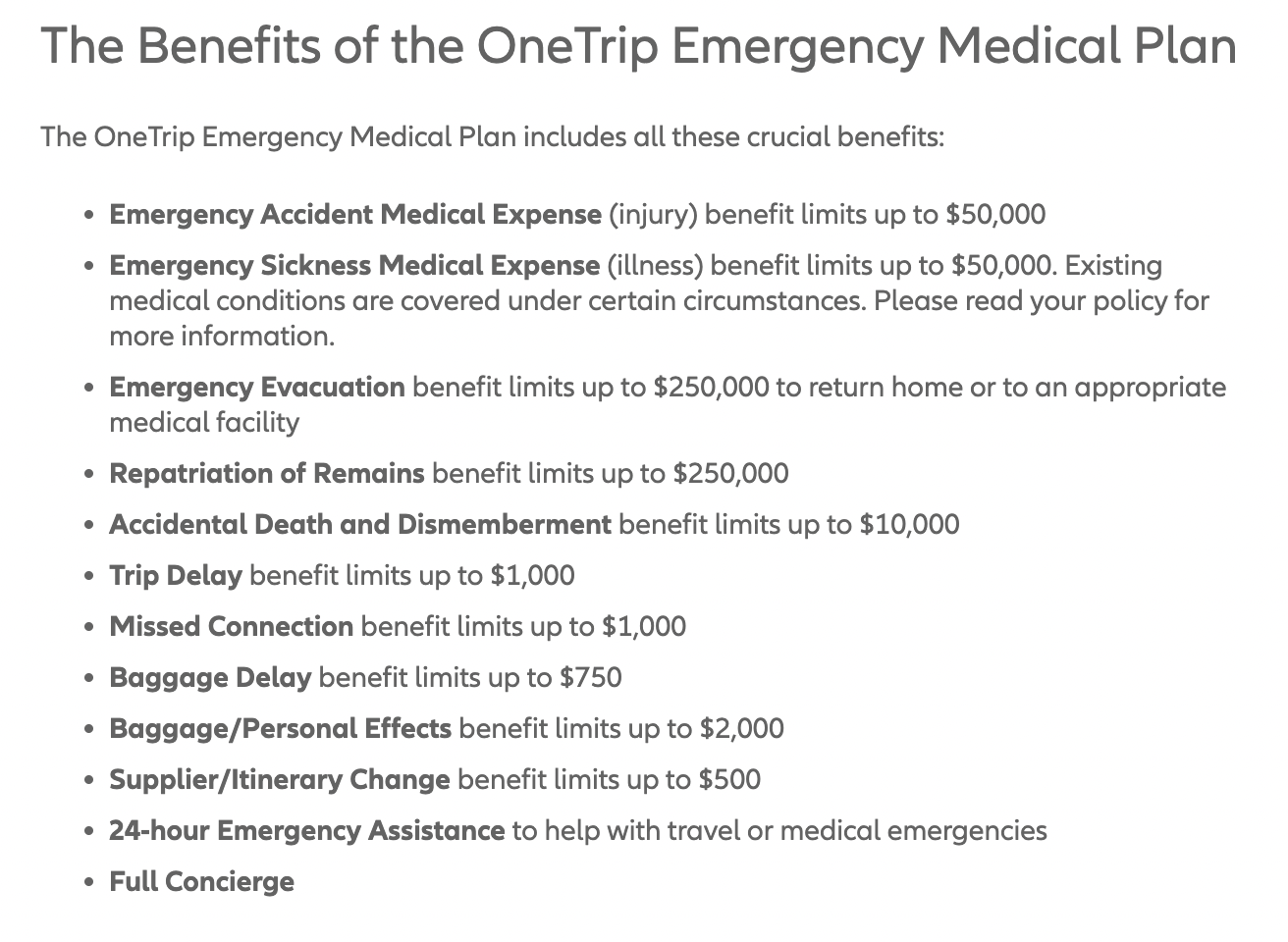

OneTrip Emergency Medical is a great option if you’ve left on a trip, forgot to get insurance, and are looking for a way to have coverage in a foreign country. Here’s a list of the benefits included pre + post departure.

Medical was my primary concern

While it may suck to lose a bag, get delayed, or lose a hotel deposit…getting hit with a life threatening illness or a huge medical bill while abroad was my primary concern. I also have a few different credit cards that will provide lost baggage, trip delay, etc so it’s not my primary concern. Years ago, while in South Africa my mother fell in the hotel room, and ended up breaking her wrist. Her travel insurance not only reimbursed her for all medical expenses while in South Africa, it also covered the bills in the States, including Physical Therapy.

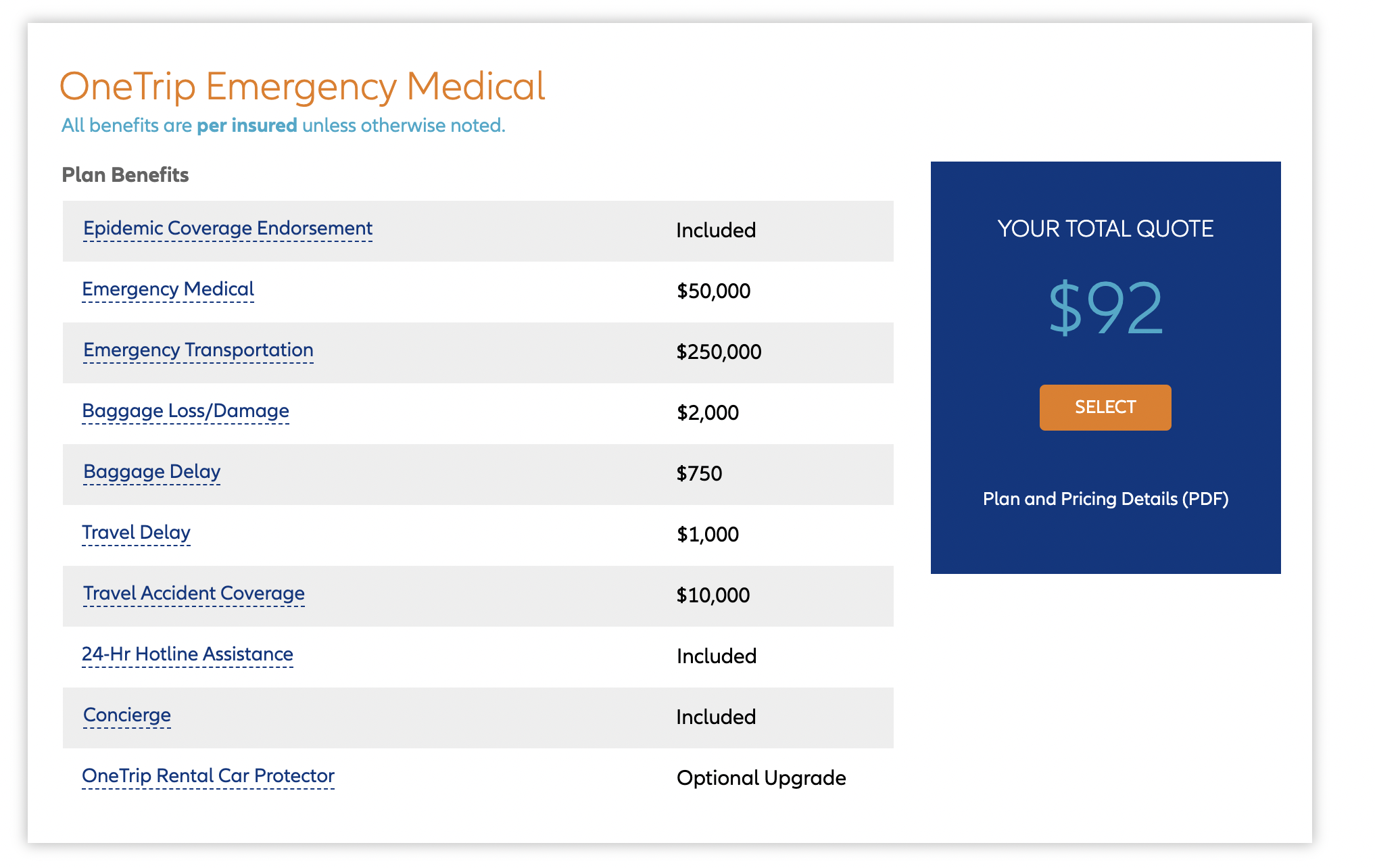

I priced out a trip for my wife and I later this year that may last up to a month and take us around the world. It’ll mostly be covered with points, but I put the other values at $2500. The travel insurance was $92 and covered both of us. A complete no brainer for us and something we will most definitely do, especially in the time of Covid. As you can see…epidemic coverage is included.

Year long plans

Year long plans

I keep a year long plan, and one thing to keep in mind, depending on the plan you get, is that medical may not apply if you stay in a country longer than 30 days. This would potentially be the case if you rent a car longer than that period of time on a single rental as well. This tends to change from plan to plan and country to country as each one defines “resident” or “lease” a little differently. Just things to keep I mind as you’re planning your trip.

This is the cost for me to have a year long, top tier, plan = $484

I use GeoBlue Trekker Choice for year long medical coverage

I use GeoBlue Trekker Choice for year long medical coverage

Compared to the AllTrips above, the GeoBlue plans are very thorough on medical, with much higher maxmimums on evac, ability to use BlueCross Blue Shield networks of doctors, etc.

Do Credit Cards come with any protection?

Yes, and most notably, Amex Platinum comes with evacuation insurance ( you can read the full benefit here – and yes, it’s valid even if you don’t pay for your trip with the card, and includes covered family members, and has no cap ).

Yes, I have an Amex Platinum, but for $92 this would not only provide medical evac, but it would include emergency medical insurance.

Chase Sapphire Reserve® also comes with Medical Evac ( up to $100k ).

Overall

My personal concerns are medical coverage, so that’s where I focus my coverage, but if you are more concerned about cancellation, etc I would certainly look at your credit card coverage and see how that compares to what the paid plans cover. A lot of cards provide excellent delay and cancellation coverage.

Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

The responses below are not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved, or otherwise endorsed by the bank advertiser. It is not the bank advertiser's responsibility to ensure all posts and/or questions are answered.